Expert Comment: Metro Bank - A detailed analysis of strategic choices and outcomes

University of Salford Business School’s Dr Zeeshan Syed, Lecturer in Finance, shares his thoughts on Metro Bank financial Strategies and outcomes.

Firstly, it's important to note that Metro didn't necessarily "fail" but got caught in the trap of its own ambitions. Metro Bank started as a challenger to reinvent the British Banking landscape by becoming a “bank next door”. The idea is simple but is far from the ex-post-financial crisis realities and the emergence of fintech. In the time when established banks were striving to cut costs, lower the provision of bad debts, and were trying to gain operational efficiency through technology, Metro took the opposite direction, which is as follows:

- It developed a highly expensive branch system.

- It relied on interest income generated through the spread between deposit plus borrowing costs and interest income from lending.

- It used high-quality bonds as safety assets deposited with the Bank of England.

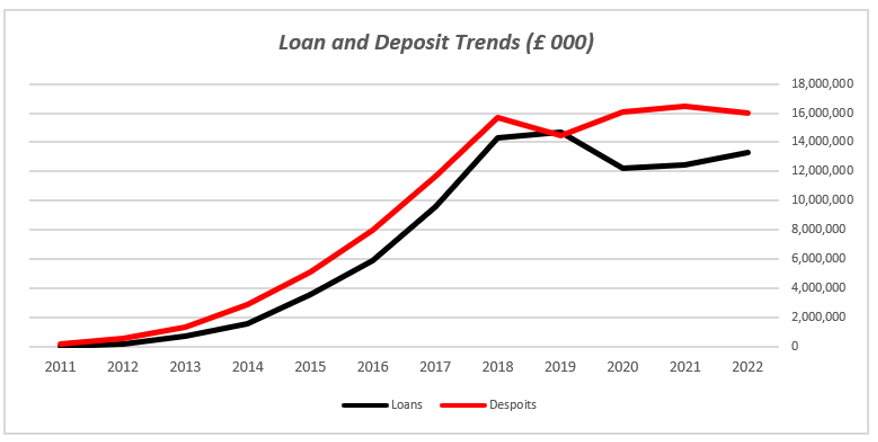

One might question the efficacy of these steps. While there isn't a straightforward answer, observing certain trends can provide insights. Metro Bank operates as a deposit-intensive bank, and from the start, it aimed to leverage the depositor's fund to finance their income-generating assets. Current and low-interest-rate savings accounts did a fantastic job financing Metro’s plan. As shown below, the bank's loan and deposit books closely followed each other. Therefore, Metro, from the very start, tried to lend as much as it could using its customers' deposits. The strategy worked until 2019 when it became apparent that the bank was poorly prepared to handle systemic shocks such as COVID-19. It's also noticeable that Metro was always a capital-deficient bank that believed its “borrowers will pay on time and in full”. Banking does not operate this way; banks must have surplus capital to account for bad debt, defaults and unforeseen systemic events.

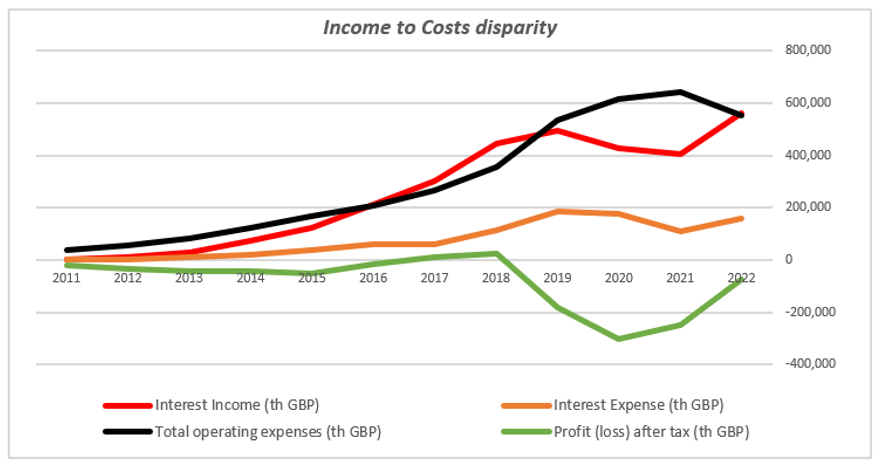

Being an ambitious bank is fine, but whether this strategy generates enough net interest income to cover interest and operating expenses is challenging. The answer is no. Metro could cover its interest expenses, but its overreliance on branch banking and operational inefficiency made it a loss-making bank. Apart from 2016 to 2019, the bank never covered its operational costs plus interest expenses through its interest income. Since 2018, the bank has been making significant losses.

Not only is Metro operationally inefficient, but it is also a victim of recent economic calamities. Rising interest rates have lowered the values of its safer assets, such as bonds. These bonds are deposited with the Bank of England to cover its capital charge requirements. However, due to the decreased value of bonds, Metro Bank must top up their capital reserve to remain aligned with the Bank of England's regulatory requirements. In fact, apart from 2018 and 2019, Metro never touched the 13% benchmark for Tier 1 capital ratio.

A bank whose assets are losing value, customers whose savings are decreasing, and borrowers whose ability to pay is becoming questionable due to a cost-of-living crisis is heading for a blood bath. As Sir John Maynard Keynes said, when facts change, change your mind or for Metro, change your ambitions.

For all press office enquiries please email communications@salford.ac.uk.